Shareholder Agreements in Japan: Protecting Your Interests in a Startup Venture

Learn how a Shareholder Agreement under Japanese law can safeguard investor rights, structure governance and secure exit options in startup ventures. Key clauses, recent case law and drafting tips inside.

TL;DR

A well‑drafted Shareholder Agreement (SHA) is essential for venture investors in Japan. It supplements the Companies Act and Articles of Incorporation by confidentially allocating governance rights, transfer restrictions, financing protections and exit mechanisms. Recent court decisions confirm enforceability of voting arrangements, making SHAs a powerful risk‑mitigation tool.

Table of Contents

- The Purpose and Legal Standing of Shareholder Agreements in Japan

- Key Provisions Commonly Found in Japanese Startup SHAs

- Governance and Management Rights

- Share Transfer Restrictions

- Capital Structure and Future Financing

- Exit Strategies

- Voting Agreements

- Founder‑Specific Clauses

- Deadlock Resolution

- Shareholder Agreement vs. Articles of Incorporation (Teikan)

- Drafting and Negotiating SHAs in Japan: Practical Tips

- Enforcement and Remedies

- Conclusion

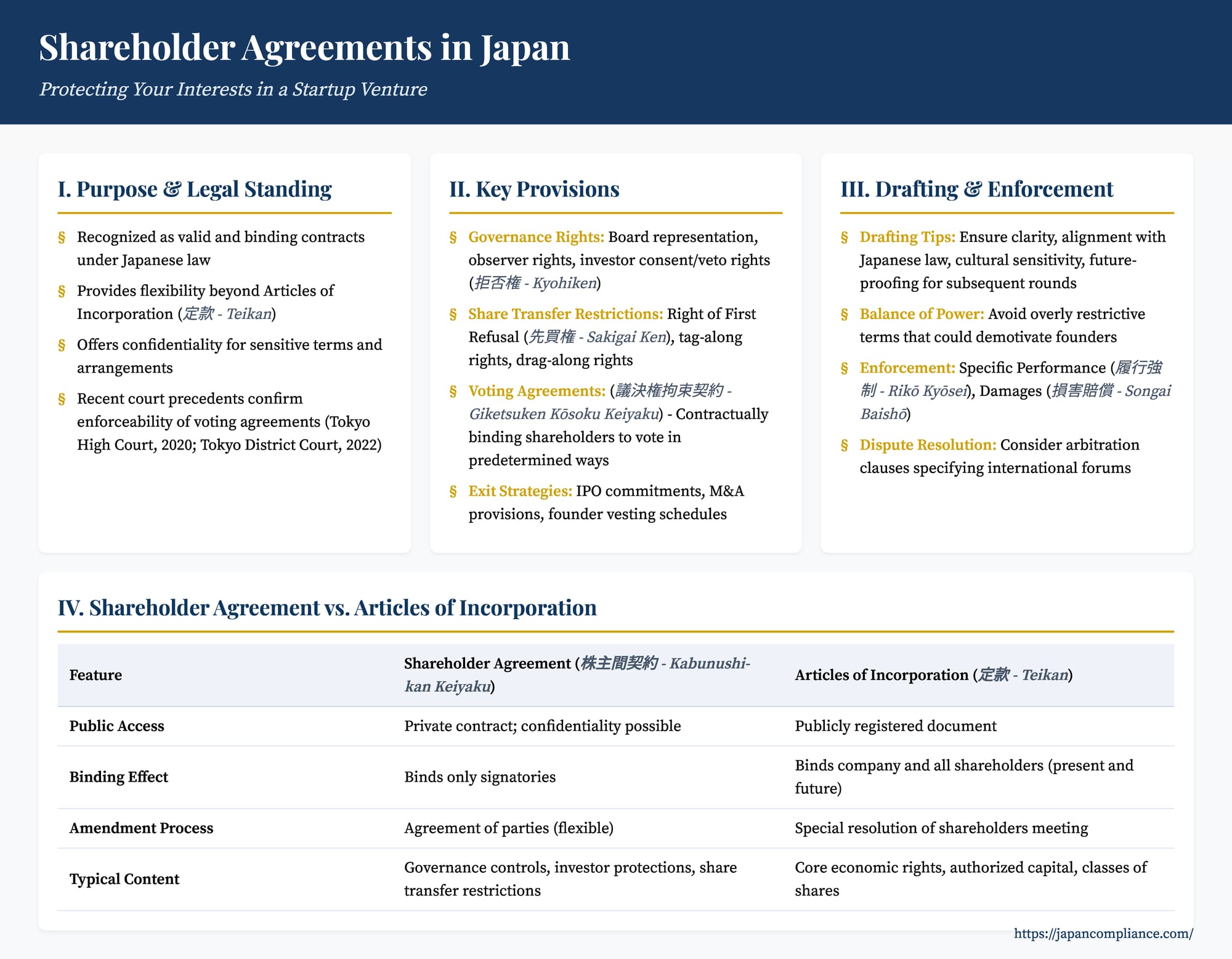

Investing in a Japanese startup, like any venture investment, requires careful legal groundwork to protect investor interests and align shareholder expectations. While the company's Articles of Incorporation (定款 - Teikan) and the Japanese Companies Act (会社法 - Kaisha-hō) provide a foundational legal framework, the Shareholder Agreement (SHA) (株主間契約 - Kabunushi-kan Keiyaku) often serves as the critical document for tailoring governance, share transfer rights, and other bespoke arrangements among founders, investors, and other key shareholders. For U.S. investors, understanding the role and common provisions of SHAs in the Japanese context is vital for successful engagement.

The Purpose and Legal Standing of Shareholder Agreements in Japan

Japanese startups, particularly those backed by venture capital or multiple investors, frequently utilize SHAs. The primary reason is the need for specific contractual arrangements that go beyond, or modify, the default rules provided by the Companies Act or what is typically included in the publicly registered Articles of Incorporation. SHAs offer flexibility and confidentiality for sensitive terms that parties may not wish to disclose publicly.

In principle, SHAs are recognized as valid and binding contracts under Japanese law, subject to general contract principles and public policy considerations. Their enforceability, particularly specific performance of certain clauses like voting agreements, has been increasingly affirmed by Japanese courts, lending greater certainty to these crucial instruments. However, it's important that SHAs do not unduly restrict the statutory rights of shareholders or the fiduciary duties of directors in a way that contravenes mandatory provisions of the Companies Act or public order.

Key Provisions Commonly Found in Japanese Startup SHAs

While the specifics of an SHA will vary based on the deal, several types of provisions are commonly encountered when investing in Japanese startups:

1. Governance and Management Rights

These clauses aim to give investors a say in the company's strategic direction and oversight.

- Board Representation (取締役選任権 - Torishimariyaku Senninken): Investors often negotiate the right to appoint one or more directors to the startup's board. This can be a direct appointment right or an agreement among shareholders to vote their shares in favor of the investor's nominee.

- Observer Rights: If a board seat is not granted, an investor might secure the right to appoint an observer to attend board meetings, allowing them to stay informed even without direct voting power at the board level.

- Investor Consent / Veto Rights (拒否権 - Kyohiken): SHAs frequently list specific material corporate actions that require the prior consent of the investor or a special majority of shareholders (which includes the investor). These often include:

- Issuance of new shares or securities convertible into shares.

- Amendments to the Articles of Incorporation.

- Significant acquisitions or disposals of assets.

- Changes in the nature of the business.

- Incurring debt above a certain threshold.

- Declaration of dividends.

- Approval of annual budgets and business plans.

These rights are critical for protecting investors from unilateral decisions by management or majority shareholders that could adversely affect their investment. While some veto rights can be embedded as class share rights in the Articles of Incorporation, many startups and investors prefer the confidentiality and flexibility of contractual SHAs for these detailed operational controls.

- Information Rights (情報取得権 - Jōhō Shutokuken): Investors typically require rights to access company information, such as periodic financial statements, management reports, and budgets, to monitor their investment and the company's performance.

2. Share Transfer Restrictions

To ensure stability and control over the shareholder base, SHAs almost always include restrictions on the transfer of shares.

- Right of First Refusal (ROFR) (先買権 - Sakigai Ken): If a shareholder wishes to sell their shares, they must first offer them to the other existing shareholders (or a designated group, like investors) on the same terms offered by a third-party buyer.

- Right of First Offer (ROFO): Requires a selling shareholder to first offer shares to other shareholders before seeking a third-party buyer.

- Co-Sale (Tag-Along) Rights (共同売却権 - Kyōdō Baikyaku-ken): Allows minority shareholders (typically investors) to participate in a sale of shares by founders or other major shareholders on a pro-rata basis, ensuring they get an opportunity to exit alongside larger shareholders.

- Drag-Along Rights (強制売却権 - Kyōsei Baikyaku-ken): Enables majority shareholders (often including investors post-consolidation of shares) to force minority shareholders to sell their shares to a third-party acquirer if a certain threshold of shareholders approves the sale. This is crucial for facilitating M&A exits.

- Lock-up Provisions: Restrictions on selling shares for a specified period, often applicable to founders and sometimes early investors, especially in the lead-up to an IPO.

3. Capital Structure and Future Financing

- Pre-emptive Rights (新株引受権 - Shinkabu Hikiuke-ken): The right for existing shareholders to subscribe to new share issuances on a pro-rata basis, allowing them to maintain their percentage ownership and avoid dilution.

- Anti-Dilution Provisions (希薄化防止条項 - Kihakuka Bōshi Jōkō): These are more commonly detailed in the terms of preferred shares within the Articles of Incorporation but can be referenced or reinforced in the SHA. They protect investors if the company issues shares at a price lower than what the investor paid (a "down round").

4. Exit Strategies

SHAs often include provisions to facilitate investor exits.

- IPO-Related Clauses: Commitments from the company and founders to pursue an IPO within a certain timeframe, cooperation in the IPO process, and agreements on the conversion of preferred shares to common stock upon a qualifying IPO.

- M&A Provisions: As mentioned, drag-along and tag-along rights are key for M&A exits. SHAs might also specify processes for evaluating M&A offers.

5. Voting Agreements (議決権拘束契約 - Giketsuken Kōsoku Keiyaku)

A particularly important aspect of Japanese SHAs is the use of voting agreements, which contractually bind shareholders to vote their shares in a predetermined manner on specific matters. This is a powerful tool for structuring control and ensuring strategic alignment.

- Enforceability at Shareholder Meetings: Japanese law generally recognizes the validity of agreements among shareholders on how to exercise their voting rights at general meetings. Historically, there was some debate on the specific enforceability (i.e., whether a court would compel a shareholder to vote in accordance with the agreement or merely award damages for breach). However, recent court precedents have strengthened the view that such agreements are specifically enforceable. For instance, a Tokyo High Court decision on January 22, 2020, dealt with the validity and duration of such agreements. More directly relevant to startups, a Tokyo District Court preliminary injunction decision on June 24, 2022 (Reiwa 4), affirmed the enforceability of a voting agreement within a startup SHA context concerning director appointments.

- Enforceability at Board Meetings: SHAs may also extend to agreements on how directors nominated by certain shareholders should vote at board meetings, particularly concerning the appointment of a representative director. While directors have fiduciary duties to the company, agreements guiding their votes within the scope of their discretion (and not conflicting with their duties) are increasingly seen as permissible. A Tokyo District Court decision on July 26, 2022 (Reiwa 4), in the substantive proceedings following the aforementioned preliminary injunction, touched upon the obligations of shareholders to ensure their nominated directors vote in line with SHA provisions regarding the appointment of a representative director.

The ability to enforce these voting agreements provides significant comfort to investors relying on them to secure board representation or influence key corporate decisions.

6. Founder-Specific Clauses

- Vesting of Founder Shares: To incentivize founders to remain with the company, their shares may be subject to vesting schedules, where full ownership is earned over time or upon achieving certain milestones.

- Key Person Clauses: Requiring key founders to remain actively involved in the business for a specified period.

- Restrictions on Founder Resignation (辞任の制限 - Jinin no Seigen): SHAs sometimes include clauses where founders agree not to resign from their directorships or key management positions without investor consent or for a certain period. The enforceability of such personal undertakings against public policy (freedom to choose one's occupation) needs careful consideration, but within reasonable limits, especially when tied to the investment rationale, they may be upheld contractually between the parties. A founder breaching such a clause could face contractual damages, even if specific performance (forcing them to stay) is unlikely.

7. Deadlock Resolution

Mechanisms to resolve situations where shareholders or directors are unable to agree on critical decisions (e.g., mediation, arbitration, buy-sell provisions).

Shareholder Agreement vs. Articles of Incorporation (定款 - Teikan)

A common question is which provisions should be in the SHA versus the company's Articles of Incorporation.

- Articles of Incorporation (Teikan): These are the company's constitutional documents, registered publicly. Certain fundamental matters, like the authorized capital, classes of shares and their core rights (e.g., liquidation preference, conversion rights if structured as class rights), and provisions required by the Companies Act, must be in the Teikan. Amendments to the Teikan generally require a special resolution of shareholders. Rights defined in the Teikan are binding on the company and all shareholders, present and future.

- Shareholder Agreement (SHA): An SHA is a private contract binding only on its signatories. This offers:

- Flexibility: SHAs can be more easily amended by the agreement of the parties involved without formal shareholder meeting resolutions or public registration.

- Confidentiality: Sensitive commercial terms or governance arrangements can be kept private.

- Customization: SHAs can cater to the specific needs and relationships of a particular group of shareholders (e.g., founders and a specific round of investors).

Typically, core economic rights of preferred shares (liquidation preference, dividend preference, conversion ratios) are defined in the Teikan as attributes of that class of shares. However, more nuanced governance controls, detailed investor protection provisions (like specific veto rights over operational matters), and share transfer restrictions among specific shareholders are often placed in the SHA for greater flexibility and privacy. Some investors prefer having crucial rights (like veto rights or director appointment rights) also reflected as class rights in the Teikan for stronger enforceability against the company itself, though this comes at the cost of public disclosure and less flexibility.

Drafting and Negotiating SHAs in Japan: Practical Tips

- Clarity is Key: Ensure all terms are clearly defined, especially for complex provisions like liquidation preferences or anti-dilution mechanisms. Ambiguity can lead to disputes.

- Alignment with Japanese Law: While SHAs allow for customization, they must operate within the framework of the Japanese Companies Act. Provisions that overtly contravene mandatory law may be unenforceable.

- Cultural Sensitivity: Negotiation styles in Japan can be more consensus-oriented and less confrontational than in some Western contexts. Building trust and understanding the counterparty's perspective are important.

- Balance of Power: While investors seek robust protections, an SHA that is overly restrictive or one-sided can demotivate founders and hinder the startup's growth.

- Future-Proofing: Consider how the SHA will function through subsequent funding rounds and in different exit scenarios. Will new investors be required to accede to the existing SHA?

- Use of Local Counsel: Engaging experienced Japanese legal counsel is indispensable. They can provide insights into market practices, ensure compliance with local laws, and assist in drafting culturally and legally sound agreements.

Enforcement and Remedies

If a party breaches an SHA, the non-breaching parties may seek remedies such as:

- Specific Performance (履行強制 - Rikō Kyōsei): A court order compelling the breaching party to perform their obligations. As noted, Japanese courts are increasingly willing to grant specific performance for certain SHA clauses, particularly clear-cut voting agreements.

- Damages (損害賠償 - Songai Baishō): Monetary compensation for losses incurred due to the breach.

- Injunctive Relief (差止請求 - Sashitome Seikyū): A court order prohibiting a party from taking a certain action in breach of the SHA.

However, litigation in Japan can be a lengthy process. Therefore, many SHAs include arbitration clauses, often specifying international arbitration forums, as a preferred method for dispute resolution.

Conclusion

Shareholder Agreements are indispensable tools in the Japanese startup investment landscape. They provide the critical contractual layer that allows founders and investors to define their relationship, allocate control, protect economic interests, and plan for future contingencies in ways that go beyond the standard provisions of company law and the Articles of Incorporation. For U.S. investors, a well-drafted, carefully negotiated SHA, informed by a solid understanding of Japanese legal norms and market practices, is a cornerstone of mitigating risk and maximizing the potential for a successful venture in Japan's burgeoning startup ecosystem.

- M&A in Japan: Key Corporate Governance Considerations for US Acquirers or Targets

- Navigating Share Inheritance in Japan: A Deep Dive into Co‑Ownership

- Fictitious Share Payments in Japan: Legal Consequences for Subscribers and Directors

- Guidelines for Corporate Takeovers (Ministry of Economy, Trade and Industry)

- Companies Act – Unofficial English Translation (Japanese Law Translation)