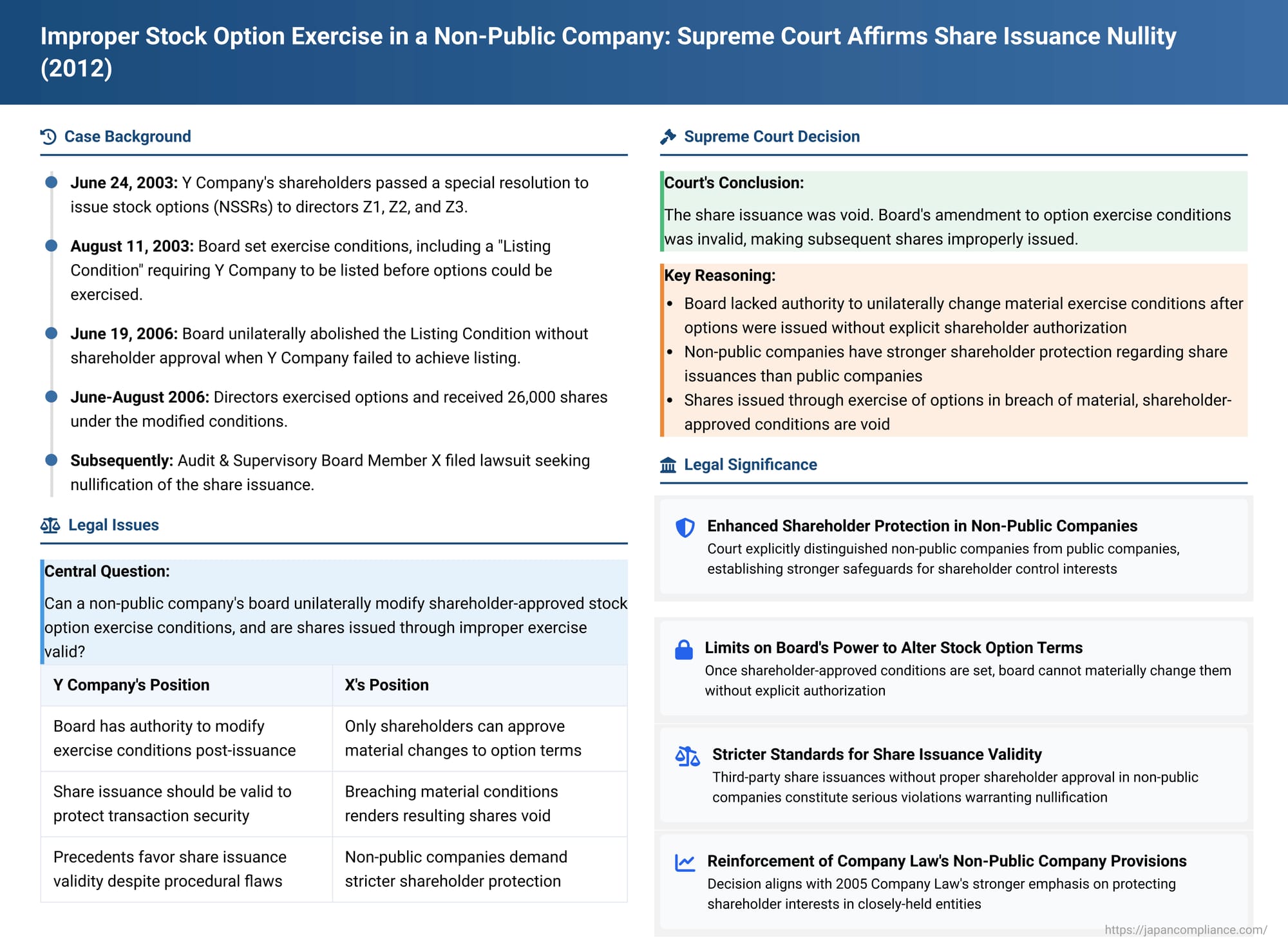

Improper Stock Option Exercise in a Non-Public Company: Japanese Supreme Court Affirms Share Issuance Nullity

Judgment Date: April 24, 2012

Case: Action for Nullity of New Share Issuance (Supreme Court of Japan, Third Petty Bench)

This 2012 Japanese Supreme Court decision provides crucial clarification on the validity of shares issued by a non-public company when those shares result from the exercise of stock options (new share subscription rights, or NSSRs) whose original, shareholder-approved exercise conditions were subsequently altered by the board of directors without explicit shareholder authorization. The Court found such share issuances to be void, emphasizing the protection of existing shareholders' interests in non-public companies.

Factual Background: Stock Options, Changed Conditions, and a Legal Challenge

The case involved Y Company, a "non-public company" (meaning all its shares were subject to transfer restrictions requiring board approval), and its directors Z1, Z2, and Z3.

- Initial Stock Option Grant: On June 24, 2003, Y Company's shareholders' meeting passed a special resolution to issue NSSRs to its directors free of charge. The stated purpose was to enhance the motivation and morale of the management team. The shareholders' resolution stipulated that a key exercise condition was that the option holder must be a director of Y Company at the time of exercise. Other exercise conditions were to be determined by a board of directors' resolution and set forth in individual NSSR allotment agreements between Y Company and the recipient directors.

- Board-Set Exercise Condition (Listing Condition): On August 11, 2003, Y Company's board of directors resolved to allot these NSSRs to directors Z1, Z2, and Z3. The ensuing allotment agreements included an important exercise condition, referred to as the "Listing Condition." This condition stipulated that the NSSRs could not be exercised until six months after Y Company's shares were either registered for over-the-counter trading or listed on a recognized stock exchange. Y Company then formally issued the NSSRs with these terms.

- Difficulties and Change of Conditions: Subsequently, Y Company encountered difficulties with its plans to go public. On June 19, 2006, Y Company's board of directors passed a new resolution (the "Amending Resolution") which purported to abolish the Listing Condition. On the same day, Y Company and directors Z1, Z2, and Z3 entered into agreements to amend their original NSSR allotment contracts to reflect this removal of the Listing Condition.

- Exercise of Options and Share Issuance: Between June and August 2006, directors Z1, Z2, and Z3 exercised their NSSRs. Consequently, Y Company issued a total of 26,000 new common shares to them (the "Share Issuance").

- Legal Action by Audit & Supervisory Board Member: X, an Audit & Supervisory Board Member (監査役 - kansayaku) of Y Company, filed a lawsuit to have the Share Issuance declared void under Article 828(1)(ii) of the Company Law. X's central argument was that the Amending Resolution by the board was invalid. Therefore, the exercise of the NSSRs by Z1-Z3, which relied on this invalid amendment, was in breach of the original, lawfully established exercise conditions, rendering the subsequent Share Issuance void.

- Lower Court Rulings: Both the Tokyo District Court (first instance) and the Tokyo High Court (appellate instance) ruled in favor of X, finding the Share Issuance void. Y Company then appealed this decision to the Supreme Court.

The Supreme Court's Judgment: Share Issuance Deemed Void

The Supreme Court dismissed Y Company's appeal, upholding the lower courts' decisions that the Share Issuance was void. The Court's reasoning involved several key steps:

Part I: Invalidity of the Board's Amending Resolution (Under Old Commercial Code Principles)

Since the NSSRs were initially issued before the current Company Law came into effect (May 1, 2006), the validity of the board's authority to set and amend conditions was assessed under the principles of the old Commercial Code.

- The Court reasoned that when a shareholders' meeting (under the old Commercial Code Art. 280-21(1)) delegates to the board the power to determine NSSR exercise conditions, this delegation is implicitly to set conditions appropriate based on the circumstances existing at the time of the shareholders' meeting.

- Such a delegation does not, in the absence of explicit authorization from the shareholders, grant the board the power to substantively change those conditions after the NSSRs have been issued.

- To materially alter board-set exercise conditions post-issuance would be tantamount to issuing entirely new NSSRs, an act which itself would require a fresh shareholders' resolution. Allowing the board to do so unilaterally would contravene the legislative intent of requiring shareholder approval for the issuance of NSSRs.

- Conclusion for Part I: The Supreme Court held that unless the shareholders' meeting explicitly empowered the board to subsequently amend the exercise conditions it established, a board resolution that materially changes such conditions after the NSSRs are issued is generally void (an exception might be for minor, non-substantive, or "detailed item-like" - 細目的 - changes). In this case, the 2003 shareholders' resolution contained no such explicit authorization for later amendment by the board. The abolition of the Listing Condition was clearly not a minor change. Therefore, the board's Amending Resolution seeking to abolish the Listing Condition was deemed void.

Part II: Invalidity of Share Issuances in Non-Public Companies Lacking Proper Shareholder Approval (Under Current Company Law Principles)

As the actual Share Issuance occurred after the Company Law came into effect, its validity was assessed under current Company Law.

- The Court highlighted key distinctions in how the Company Law treats share issuances by "public companies" versus "non-public companies."

- For non-public companies:

- The authority to determine the terms of a new share offering is not inherently vested in the board of directors. To issue new shares to persons other than existing shareholders (i.e., a third-party allotment), a special resolution of the shareholders' meeting is generally required to decide these terms (unless this authority has been specifically delegated to the board for a particular offering, as per Company Law Art. 199).

- The statutory period for filing a lawsuit to nullify a share issuance is longer for non-public companies (one year) compared to public companies (six months), as per Company Law Art. 828(1)(ii).

- These legislative distinctions, the Court reasoned, indicate that for non-public companies, the law places a strong emphasis on protecting the existing shareholders' interests in maintaining their shareholding ratios, which are directly linked to control of the company. The legislative intent is to provide relief through nullification suits if shares are issued contrary to the will of the existing shareholders.

- Conclusion for Part II: Therefore, the Supreme Court established that if a non-public company issues shares via a third-party allotment without obtaining the requisite special shareholders' resolution, this constitutes a serious procedural violation and is a ground for invalidating the share issuance. The Court explicitly distinguished this from older precedents that had been more lenient towards issuances by public companies lacking shareholder resolutions, deeming those precedents inapplicable to non-public companies.

Part III: Invalidity of Shares Issued from Exercising NSSRs in Breach of Material, Shareholder-Approved Conditions in a Non-Public Company

Connecting the above principles, the Court addressed the core issue:

- If a non-public company issues NSSRs to non-shareholders based on a shareholders' resolution that includes specific exercise conditions (or validly delegates the setting of such conditions), and these conditions are material to the purpose for which the NSSRs were issued:

- Then, the issuance of new shares resulting from the exercise of these NSSRs in direct contravention of such material conditions leads to a situation where existing shareholders' shareholding ratios are affected against their will. This outcome is substantively no different from the company directly issuing new shares via a third-party allotment without a proper special shareholders' resolution.

- Conclusion for Part III: Consequently, the issuance of shares based on the exercise of NSSRs in breach of material, shareholder-approved (or validly board-set under shareholder delegation) exercise conditions is also a ground for invalidating that share issuance in a non-public company.

- In this specific case, the Listing Condition was established based on authority delegated by the shareholders' meeting and was clearly linked to the NSSRs' purpose of motivating management towards achieving a public listing. Thus, it was a material condition. Since the Amending Resolution to abolish it was void, the subsequent exercise of the NSSRs and the resulting Share Issuance were in breach of this material condition and therefore had a ground for invalidity.

Analysis and Implications: Strengthening Shareholder Rights in Non-Public Companies

This 2012 Supreme Court decision carries significant weight, particularly for the corporate governance of non-public companies in Japan.

- Board's Limited Power to Alter NSSR Conditions: The ruling firmly establishes that in a non-public company, once NSSR exercise conditions have been set pursuant to shareholder approval (even if via delegation to the board under older laws), the board cannot unilaterally make material changes to these conditions after the NSSRs have been issued, unless the shareholders explicitly granted such amendment power. The current Company Law (Art. 239(1)(i)) further reinforces this by generally not allowing the content of NSSRs, which includes exercise conditions, to be delegated by shareholders to the board for determination in non-public companies.

- Nullity of Unauthorized Share Issuances in Non-Public Companies: This decision was a landmark in clarifying that, for non-public companies, the issuance of new shares to third parties without a valid special shareholders' resolution is a serious enough defect to render the issuance void. This marked a departure from earlier precedents that were often more hesitant to invalidate share issuances due to procedural flaws, especially in the context of public companies operating under the authorized capital system where boards had more inherent issuance authority. The Supreme Court specifically recognized the distinct nature of non-public companies, where shareholder control and the existing shareholder composition are of paramount importance.

- Breach of Material Exercise Conditions Leads to Void Share Issuance: Critically, the Court extended this principle to shares issued upon the exercise of NSSRs. If material, shareholder-approved exercise conditions are breached, the resulting shares are tainted with an invalidity ground. This prevents circumvention of shareholder will through the two-step process of issuing NSSRs and then improperly altering their terms before exercise.

- Justice Terada's Supplementary Opinion: An insightful supplementary opinion by Justice Terada (with Justice Otani concurring) provided a detailed historical and philosophical context. It traced the evolution of Japanese company law, highlighting the increasing recognition of the special characteristics of non-public companies and the strengthening of shareholder rights within them, particularly concerning share and NSSR issuances. Justice Terada viewed the directors' actions in this case as a direct affront to this established legal trend and suggested that under the current Company Law, there is arguably no room for a board of a non-public company to determine or alter material NSSR exercise conditions at all.

Conclusion: Upholding Shareholder Intent in Non-Public Company Stock Options

The Supreme Court's 2012 decision significantly bolsters shareholder protection in Japanese non-public companies. It makes clear that shareholder-approved terms for stock options, especially material exercise conditions, cannot be easily cast aside by director-level decisions. Furthermore, it solidifies the principle that unauthorized share issuances that dilute existing shareholders or alter control structures against the democratically expressed will of the shareholders (via a special resolution) are liable to be nullified. This ruling underscores the importance of adhering strictly to shareholder mandates when dealing with equity-linked incentives and capital increases in the context of closely-held corporations.