Front Row Ruckus: Japanese Supreme Court on Preferential Seating at AGMs and Shareholder Equality

Date of Judgment: November 12, 1996

Court: Supreme Court of Japan, Third Petty Bench

Introduction

Shareholder Annual General Meetings (AGMs) can sometimes be contentious forums, especially for companies dealing with controversial issues. Company management often seeks to ensure smooth proceedings, but what happens when measures taken to control the environment are perceived as discriminatory by some shareholders? This was the central theme in a notable case decided by the Third Petty Bench of the Supreme Court of Japan on November 12, 1996, where an electric power company, fearing disruptions, gave its employee shareholders preferential early access to front row seats at its AGM. Other shareholders, who had arrived early hoping to secure those very seats, felt unfairly treated and brought a legal challenge.

The case highlights the delicate balance between a company's desire to maintain order at its AGM and its obligation to treat all attending shareholders equitably.

The Core Principle: Equal Treatment of Shareholders at AGMs

A fundamental expectation in corporate governance is that a company should treat all shareholders attending the same AGM in an identical manner. This principle of equal treatment is paramount. However, it is not absolute; differential treatment might be permissible if there is a "reasonable justification" for it. The crux of many disputes in this area lies in what constitutes such a reasonable justification and whether the company's actions, even if well-intentioned, cross the line into inappropriate discrimination.

Facts of the Y Co. Case

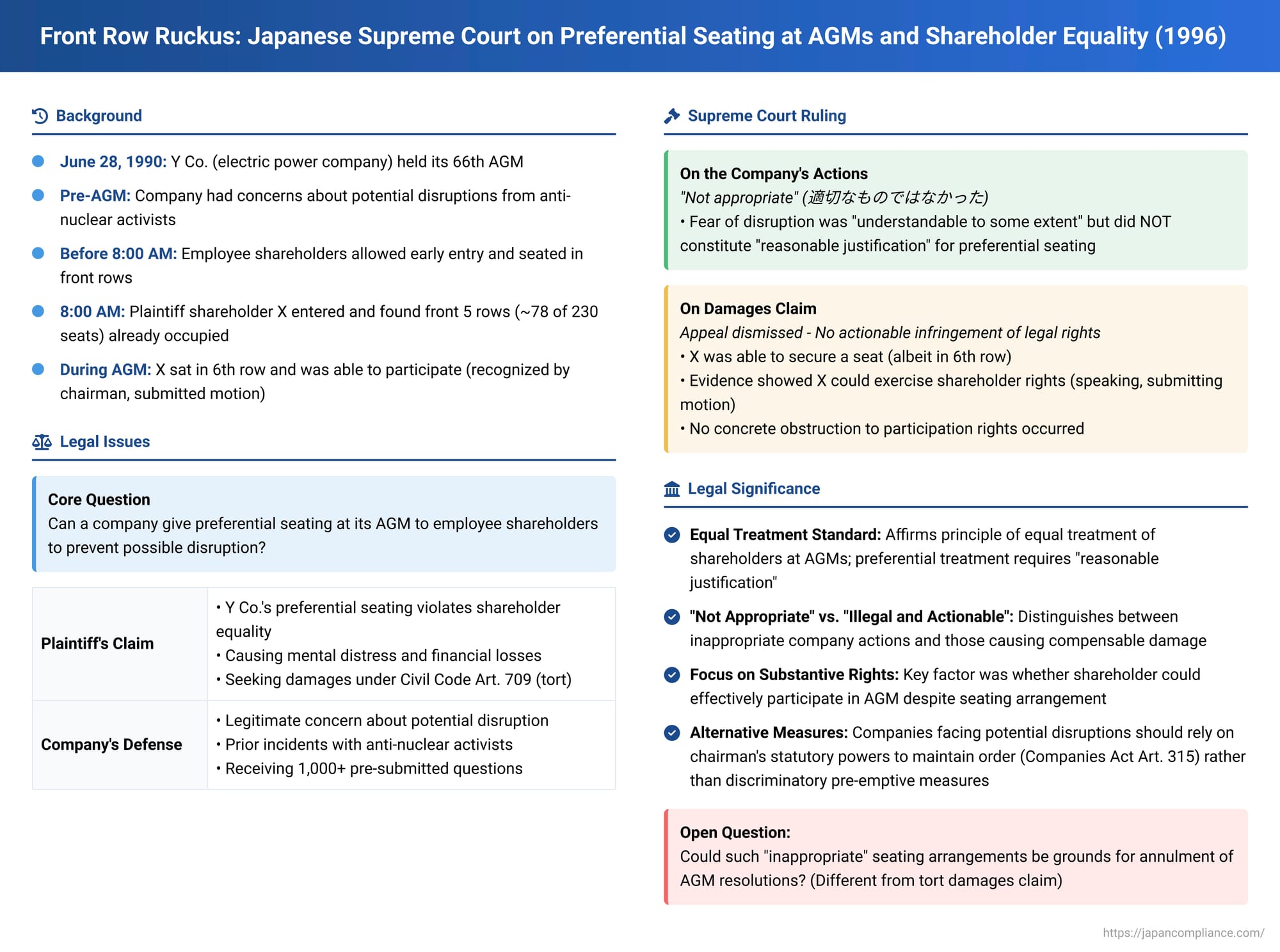

The defendant, Y Co., was an electric power company facing significant opposition regarding its nuclear power policies.

- Anticipation of a Difficult AGM: Leading up to its 66th AGM on June 28, 1990, Y Co. had reasons to be apprehensive.

- In January and February 1988, its head office building had been surrounded and partially occupied for several hours by anti-nuclear activists.

- Before the 1990 AGM, the company had received a list of over 1,000 questions from shareholder groups, including one named "Shikoku Electric Shareholders' Association for a Nuclear-Free Future".

- Given this history, Y Co. feared that the AGM proceedings might be obstructed, or that the chairman's seat and executive officers' area could be surrounded by protestors.

- Y Co.'s Pre-emptive Seating Arrangement: To mitigate these perceived risks, Y Co. instructed its employee shareholders to enter the AGM venue (located in its head office building) before the official 8:00 AM opening time for general shareholders. These employee shareholders were then seated in the front rows of the venue.

- The Plaintiff Shareholders' Experience: Mr. X (T.T. in the judgment), one of the plaintiff shareholders, along with other shareholders opposed to Y Co.'s nuclear policies, had lined up early in the morning outside the venue, hoping to secure good seats. When the doors opened at 8:00 AM and they entered, they found that employee shareholders already occupied most of the first five rows and some seats in the central area, totaling approximately 78 of the roughly 230 available seats. Mr. X managed to get a seat in the sixth row, near the center.

- Participation in the AGM: Despite not getting his preferred seat, Mr. X did participate in the AGM. He was recognized by the chairman and successfully submitted one motion during the proceedings.

- The Lawsuit: Mr. X and other shareholders sued Y Co. for damages under tort law (Civil Code Article 709). They argued that Y Co.'s discriminatory seating arrangement, which favored employee shareholders, prevented them from securing their desired seats. This, they claimed, caused them mental distress and financial losses, such as accommodation costs incurred by arriving early.

The Supreme Court's Decision (November 12, 1996)

The Supreme Court delivered a nuanced judgment, addressing both the appropriateness of the company's actions and the question of whether the plaintiffs had suffered an actionable legal injury.

Company's Action Deemed "Not Appropriate"

The Court first considered the justification for Y Co.'s preferential seating arrangement.

- It acknowledged that Y Co.'s apprehension about potential disruptions at the AGM, given the past activities of anti-nuclear protestors and the barrage of pre-submitted questions, was "understandable to some extent".

- However, the Court explicitly stated that this fear did not constitute a "reasonable justification" for the specific measure taken – that is, allowing employee shareholders early entry to occupy the front seats.

- The Supreme Court concluded that Y Co.'s measure was "not appropriate" (適切なものではなかったといわざるを得ない).

This part of the ruling served as a clear rebuke of the company's chosen method for managing potential AGM disruptions, emphasizing that even legitimate concerns do not give a company carte blanche to treat shareholders unequally in terms of meeting access and seating.

No Infringement of Legal Rights Warranting Damages in This Instance

Despite finding the company's actions "not appropriate," the Supreme Court ultimately did not rule in favor of Mr. X on the claim for damages. The Court reasoned that:

- While Mr. X had lost the opportunity to sit in his preferred seat, he was still able to secure a seat in a central area of the venue.

- More importantly, the evidence showed that Mr. X was able to actively exercise his rights as a shareholder during the AGM. He was recognized by the chairman and was able to submit a motion.

- Therefore, the Court concluded that it could not be said that Mr. X's concrete exercise of shareholder rights was obstructed or hindered by Y Co.'s seating arrangements.

- As a result, no legally protected interest of Mr. X had been infringed in a way that would give rise to a claim for damages under tort law.

The appeal by Mr. X (T.T.) was dismissed. (Another appellant, S.T., had his appeal dismissed for unrelated procedural reasons regarding late filing.)

Analysis and Implications

The Supreme Court's decision in the Y Co. case offers several important takeaways:

- Judicial Scrutiny of AGM Management: The ruling signals that company actions managing AGM proceedings, especially those involving differential treatment of shareholders, are subject to judicial review for appropriateness and reasonableness. Simply fearing disruption is not enough to justify any and all pre-emptive measures.

- "Not Appropriate" vs. "Illegal and Actionable": The Court drew a distinction. While Y Co.'s preferential seating was deemed "not appropriate," this did not automatically translate into an illegal act causing compensable damage to the plaintiffs. For a tort claim to succeed, a plaintiff must demonstrate not only that the defendant's action was wrongful but also that it caused an actual infringement of a legally protected interest resulting in quantifiable damages.

- Focus on Substantive Exercise of Shareholder Rights: The key factor in denying damages seems to have been the Court's finding that Mr. X was still able to effectively participate in the AGM and exercise his core rights as a shareholder (e.g., to be present, to speak, to make motions). The inconvenience of a less preferred seat, in this specific instance, did not rise to the level of an infringement of a legal interest.

- The Principle of Shareholder Equality in AGMs: The PDF commentary on this case notes an interesting aspect: the decision appears to lean towards ensuring equality among shareholders as individuals (on a per capita basis) in the context of physical meeting arrangements, rather than the more typical understanding of shareholder equality (e.g., under Companies Act Article 109, Paragraph 1), which usually pertains to rights being proportional to the number of shares held (pro rata equality for dividends, voting power, etc.). This raises questions about the precise scope and application of "equal treatment" in the practical conduct of AGMs.

- Alternative Measures for Maintaining Order: Companies facing potentially disruptive AGMs are not without tools. The Companies Act (e.g., Article 315) grants the chairman of the AGM significant authority to maintain order, including the power to direct disruptive individuals to leave. The Supreme Court's finding that Y Co.'s pre-emptive discriminatory seating was "not appropriate" implies a preference for using such established, less discriminatory mechanisms for order maintenance if and when actual disruptions occur.

- Tort Claim vs. Annulment of AGM Resolutions: It is important to remember that this case was a claim for monetary damages based on tort law. The decision does not directly address whether such "inappropriate" seating arrangements could serve as grounds for a shareholder to sue for the annulment of resolutions passed at the AGM. Annulling resolutions would typically require proving that the procedural defect was severe enough to have potentially affected the outcome of the votes or fundamentally undermined the fairness of the meeting.

Conclusion

The 1996 Supreme Court decision in the Y Co. case confirms that while companies may have legitimate concerns about maintaining order at their AGMs, they must exercise caution and fairness in the measures they adopt. Preferential treatment, such as allowing a select group of shareholders early access to occupy prime seating, is generally considered "not appropriate," even in the face of potential protests or disruptions.

However, for a shareholder to successfully claim monetary damages arising from such inappropriate treatment, they must demonstrate more than mere inconvenience or frustration. They need to prove a concrete infringement of their legally protected rights, particularly an obstruction to their ability to effectively participate in the meeting and exercise their substantive rights as a shareholder. The case underscores the ongoing challenge for companies to balance the need for orderly and efficient AGMs with the imperative to uphold principles of fair and equal treatment for all attending shareholders.