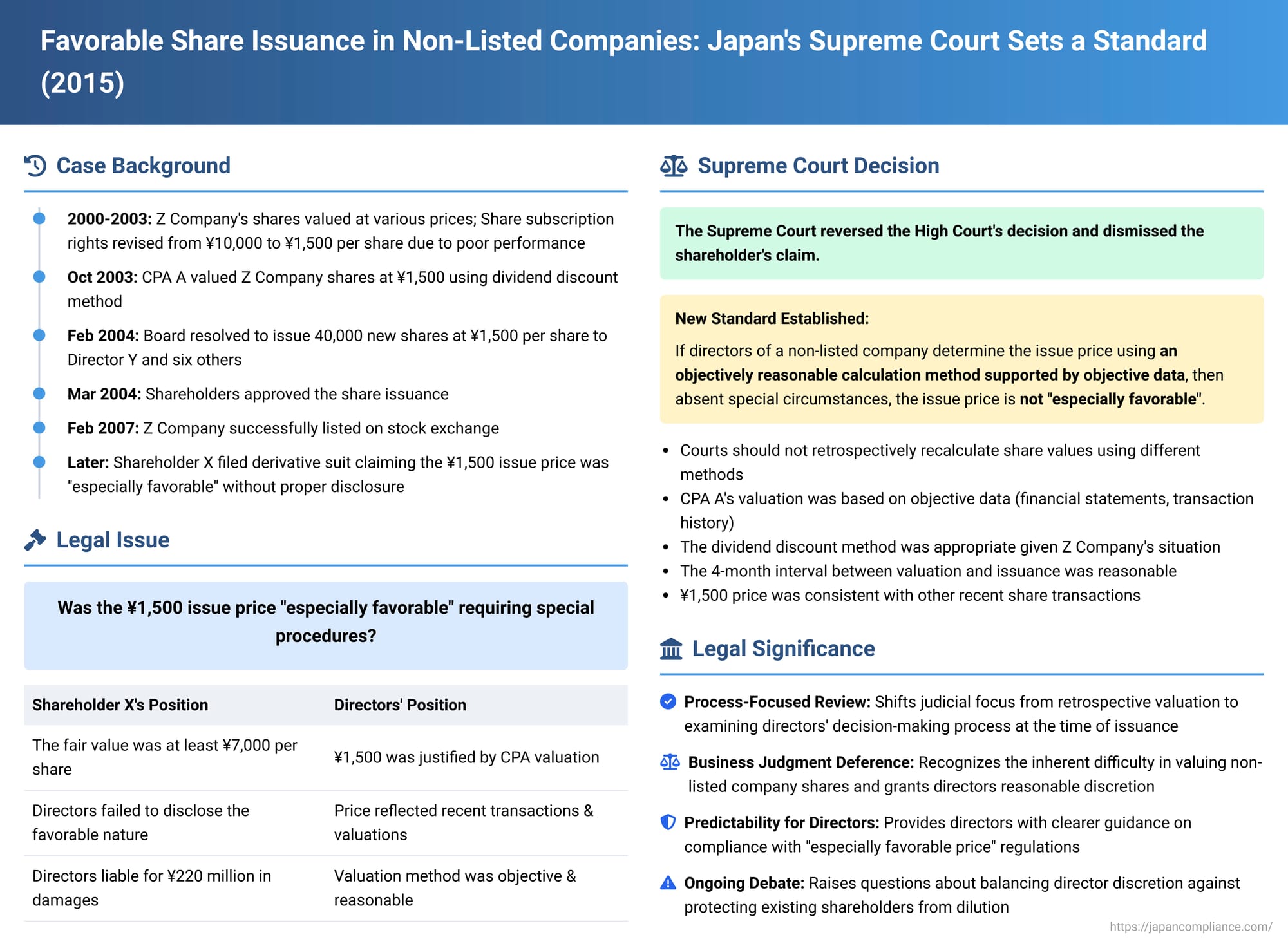

Favorable Share Issuance in Non-Listed Companies: Japan's Supreme Court Sets a Standard

Judgment Date: February 19, 2015

Case: Damages Claim (Supreme Court of Japan, First Petty Bench)

This Japanese Supreme Court decision from 2015 provides a significant benchmark for assessing whether the issue price of new shares in a non-listed company is "especially favorable" to the recipients. Such a determination has critical implications for procedural requirements under Japanese company law and the potential liability of company directors. The Court emphasized a review of the board's decision-making process at the time of issuance, rather than a retrospective judicial re-valuation of the shares.

Factual Background: A Share Issuance Under Scrutiny

The case involved Z Company, a non-listed company whose shares had transfer restrictions, operating under Japan's old Commercial Code.

- Historical Share Valuations and Transactions:

- In May 2000 (Heisei 12), the exercise price for share subscription rights attached to bonds issued by Z Company was JPY 10,000 per share.

- Due to a deterioration in business performance, this exercise price was subsequently revised in June 2003 (Heisei 15) to JPY 1,500 per share.

- Z Company's dividend per share fluctuated: JPY 150 for fiscal years 2000-2002, no dividends for fiscal years 2003-2004, JPY 100 for fiscal year 2005, and JPY 150 for fiscal year 2006.

- Beginning around 2001, several officers and key employees retired. On these occasions, their shares were purchased by the Representative Director Y (one of the appellants) and other officers at a price of JPY 1,500 per share.

- Between July and October 2002, Z Company itself repurchased some of these shares from Y at JPY 1,500 per share, holding them as treasury stock.

- In November 2003, Z Company sold these treasury shares back to Y, again at JPY 1,500 per share.

- Independent Share Valuation by CPA A:

- Prior to the November 2003 treasury stock sale, Z Company engaged CPA A to conduct a valuation of its shares.

- CPA A was provided with extensive documentation, including Z Company's financial statements for fiscal years 2000-2002, business reports, tax returns, records of past share transactions, the shareholder register, land valuation data, information on undisclosed gains or losses on assets like golf courses, and details of bad debt provisions. CPA A also confirmed in an interview that no formal business plan, which could serve as a basis for valuation, existed.

- On October 31, 2003, CPA A reported that the value of Z Company's shares was JPY 1,500 per share. The rationale provided was that the dividend discount method was most appropriate. This was based on the company's history of consistent dividend payments (despite a temporary cessation) and a pattern of share transactions occurring at prices reflecting dividend expectations.

- The Disputed New Share Issuance (March 2004):

- In February 2004, Z Company's board of directors passed a resolution to issue 40,000 new shares at an issue price of JPY 1,500 per share (totaling JPY 60 million). The payment date was set for March 24, 2004, and the shares were to be allotted to Director Y and six other individuals.

- The company did not seek a new expert valuation for this issuance. The reasoning was that it occurred within the same fiscal year as the November 2003 treasury stock sale (which used the JPY 1,500 price) and was only about four months after CPA A's valuation report.

- On March 8, 2004, a special resolution at a shareholders' meeting approved this new share issuance. During this meeting, Y and three other directors involved did not provide an explanation as to why a third-party allotment at what might be considered an "especially favorable price" was necessary.

- Subsequent Developments and Litigation:

- Z Company's financial performance subsequently improved, and its shares were successfully listed on a stock exchange in February 2007.

- X, a shareholder of Z Company, filed a shareholder derivative lawsuit against Y and other directors who were in office at the time of the March 2004 new share issuance.

- X alleged that the JPY 1,500 issue price was "especially favorable" under the then-applicable Commercial Code (Article 280-2, Paragraph 2) and that the directors had failed to provide the necessary explanation at the shareholders' meeting, thereby breaching their duties. X sought damages of over JPY 2.2 billion payable to Z Company.

- Both the Tokyo District Court (first instance) and the Tokyo High Court (appellate instance) sided with X, finding that the new share issuance was indeed at an "especially favorable price." These courts determined that the fair issue price should have been at least JPY 7,000 per share and consequently ordered the appellant directors to pay JPY 220 million in damages to Z Company. The directors then appealed this decision to the Supreme Court.

The Supreme Court's Judgment: A New Standard for Non-Listed Companies

The Supreme Court reversed the High Court's decision and dismissed X's claim against the directors.

1. The Challenge of Valuing Non-Listed Company Shares:

The Court began by acknowledging the inherent difficulties in valuing shares of non-listed companies. It noted the existence of various valuation methodologies (such as book value net asset method, market value net asset method, dividend discount method, earnings capitalization method, discounted cash flow (DCF) method, and comparable company analysis) and the lack of a definitively established standard for when to use each specific method. Furthermore, many of these methods involve subjective elements or inputs that can have a range of acceptable values, including projections of future earnings or cash flows, discount rates, and the selection of comparable companies.

2. The "Objectively Reasonable Calculation Method" Standard:

Given these valuation complexities, the Supreme Court articulated a new standard for determining whether an issue price is "especially favorable" in the context of non-listed companies:

- It is inappropriate for a court to retrospectively calculate a share price using a different valuation method or different predictive values than those used by the board, and then compare this ex-post calculation to the actual issue price to determine if it was "especially favorable." Such an approach would significantly harm the predictability for directors in making such decisions.

- Therefore, the Court held that if, at the time of issuing new shares to persons other than existing shareholders, the board of directors of a non-listed company determined the issue price based on an objectively reasonable calculation method supported by objective data, then that issue price, absent special circumstances, is not to be considered "especially favorable" (within the meaning of the Commercial Code).

3. Application to Z Company's Case:

Applying this standard to the facts:

- The Court found that CPA A's valuation was based on objective data, including Z Company's financial statements and transaction history.

- CPA A's choice of the dividend discount method, and the use of JPY 150 per share as the dividend amount (derived from past dividend payments and recent share transaction prices), could not be definitively deemed inappropriate for Z Company's situation at that time.

- The roughly four-month interval between CPA A's report and the board's resolution for the new share issuance was not considered unreasonable, as there was no evidence suggesting any events during that period that would have drastically altered Z Company's share value.

- Significantly, the Court also took into account the consistent transaction price of JPY 1,500 per share across various contexts: purchases by Director Y and other officers from retiring employees, Z Company's own treasury stock purchase and its subsequent resale to Y, Y's offer to sell shares to other key employees, and the revised exercise price of the share subscription rights.

- Considering these factors collectively, the Supreme Court concluded that the JPY 1,500 issue price for the new shares had been determined by an "objectively reasonable calculation method."

- The Court also found no "special circumstances" that would warrant a different conclusion. It specifically noted that a simple comparison of the March 2004 issue price with the company's estimated share value in May 2000 (when the company was in a different phase) or March 2006 (after its performance had significantly improved and it was heading for an IPO) was not an appropriate basis for deeming the 2004 price "especially favorable."

Consequently, the Supreme Court ruled that the JPY 1,500 issue price was not "especially favorable," and therefore, the directors were not liable.

Analysis and Implications: Balancing Director Discretion and Shareholder Protection

This 2015 Supreme Court decision is a landmark ruling for non-listed companies in Japan. It was the first time the Supreme Court had laid down a clear standard for determining an "especially favorable issue price" in this context, a concept critical for various corporate actions and potential director liabilities.

1. The "Objectively Reasonable Calculation Method" Standard:

The standard articulated by the Court shifts the focus of judicial review from a de novo (from scratch) valuation by the court to an examination of the process and basis of the board of directors' decision at the time of the share issuance. It essentially grants a degree of deference to the board's business judgment, provided their valuation method was objectively reasonable and based on concrete data.

Legal commentators have noted that this standard appears to allow for a relatively lenient review of directors' decisions. Its overall fairness and effectiveness are subjects of ongoing discussion:

- Some support it as recognizing the practical difficulties of share valuation and respecting directors' legitimate business discretion.

- Critics, however, express concern that this standard might prioritize director predictability over the protection of existing shareholders from dilution. They argue it could lead to inadequate remedies for shareholders if a truly unfair issuance is upheld simply because the board followed a superficially "reasonable" process. This approach might also seem inconsistent with the broader principle that director liability, rather than outright invalidation of the share issuance, is often considered the primary remedy for wrongfully favorable issuances.

2. Purpose of Regulating Favorable Issuances:

The underlying purpose of legal provisions against "especially favorable" share issuances is to prevent the economic dilution of existing shareholders' interests and to maintain fairness between existing and new shareholders. When new shares are issued at a price significantly below their fair value, a transfer of wealth occurs from the existing shareholders to the new allottees.

3. Conflict of Interest Considerations:

The lower courts in this case had raised concerns about a potential conflict of interest, as the directors who decided on the JPY 1,500 issue price were also among the individuals to whom the new shares were allotted. When such conflicts of interest are present, judicial scrutiny of whether an issuance is "especially favorable" should arguably be more stringent. If the standard set by the Supreme Court, or its application, is to be refined in the future, addressing how to manage or mitigate such conflicts of interest in the valuation process will be a key practical challenge for corporate governance.

4. The Nature of Loss in Favorable Issuance Cases:

A nuanced legal point is that the primary "loss" to existing shareholders from an unduly favorable share issuance is the dilution of their share value and a relative shift in wealth within the company, rather than a direct monetary loss from the company's own balance sheet in the traditional sense. While compelling directors to pay damages to the company can indirectly help restore some value to existing shareholders, the fundamental issue is the reallocation of value among different shareholder groups. The damages awarded by the lower court (JPY 220 million) differed from the estimated value of wealth transferred (approximately JPY 76 million), suggesting that framing the remedy solely as "company loss" might sometimes distort the actual economic substance of the dispute and potentially influence judicial review.

5. Scope of the Ruling:

The standard established in this case is likely to apply to share issuances by all non-listed companies under the current Company Law, irrespective of whether they are classified as "public companies" (公開会社 - kokai kaisha, meaning companies whose articles do not restrict the transfer of all shares) or "non-public/closely-held companies" (非公開会社 - hi-kokai kaisha).

Conclusion: A Framework for Assessing Share Issuances in Non-Listed Entities

The Supreme Court's 2015 judgment provides a crucial framework for evaluating the fairness of new share issue prices in non-listed Japanese companies. By focusing on whether the board of directors employed an "objectively reasonable calculation method based on objective data" at the time of the issuance, the Court offers a degree of predictability for directors. However, it also underscores the ongoing legal and academic discussion about the appropriate balance between directorial discretion in complex valuation matters and the robust protection of existing shareholders against potential dilution and unfair treatment. The "special circumstances" escape clause also leaves room for judicial intervention in exceptional cases.