Cumulative Voting and Shareholder Notices: A 1998 Japanese Supreme Court Decision on Implied Director Numbers

Date of Judgment: November 26, 1998

Court: Supreme Court of Japan, First Petty Bench

Introduction

In corporate governance, the election of directors is a fundamental shareholder right. For minority shareholders, a mechanism known as "cumulative voting" can be a vital tool to ensure representation on the board. This method allows shareholders to concentrate their voting power on a smaller number of candidates, thereby increasing the chances of electing at least one director who represents their interests. For cumulative voting to be effectively utilized, shareholders must know the precise number of directors to be elected at a given meeting.

This raises an important question regarding the information provided in the notice convening a shareholders' meeting: What happens if the notice doesn't explicitly state the number of directors to be elected? Can shareholders claim they were deprived of a fair opportunity to request cumulative voting, potentially invalidating the election results? This issue was at the center of a decision by the First Petty Bench of the Supreme Court of Japan on November 26, 1998.

The Role of Cumulative Voting and Convening Notices

Cumulative voting is a system designed to enhance minority shareholder representation. In essence, each shareholder is entitled to a number of votes equal to their number of shares multiplied by the number of directors to be elected. Shareholders can then cast all these votes for a single candidate or distribute them among several candidates. This concentration of voting power can enable a significant minority bloc to elect one or more directors, even if they do not hold a majority of the shares.

Given the mechanics of cumulative voting, the number of directors to be elected at a meeting is critically important information. Shareholders need this number to strategize their votes and to decide whether requesting cumulative voting is worthwhile or feasible. Consequently, for Japanese companies that have not excluded cumulative voting in their articles of incorporation, the general rule is that the notice convening a shareholders' meeting for the election of directors must specify the number of directors to be elected. Failure to provide this information can be considered a defect in the convening procedure and may constitute grounds for annulling the resolutions passed at that meeting.

Facts of the K Co. Case

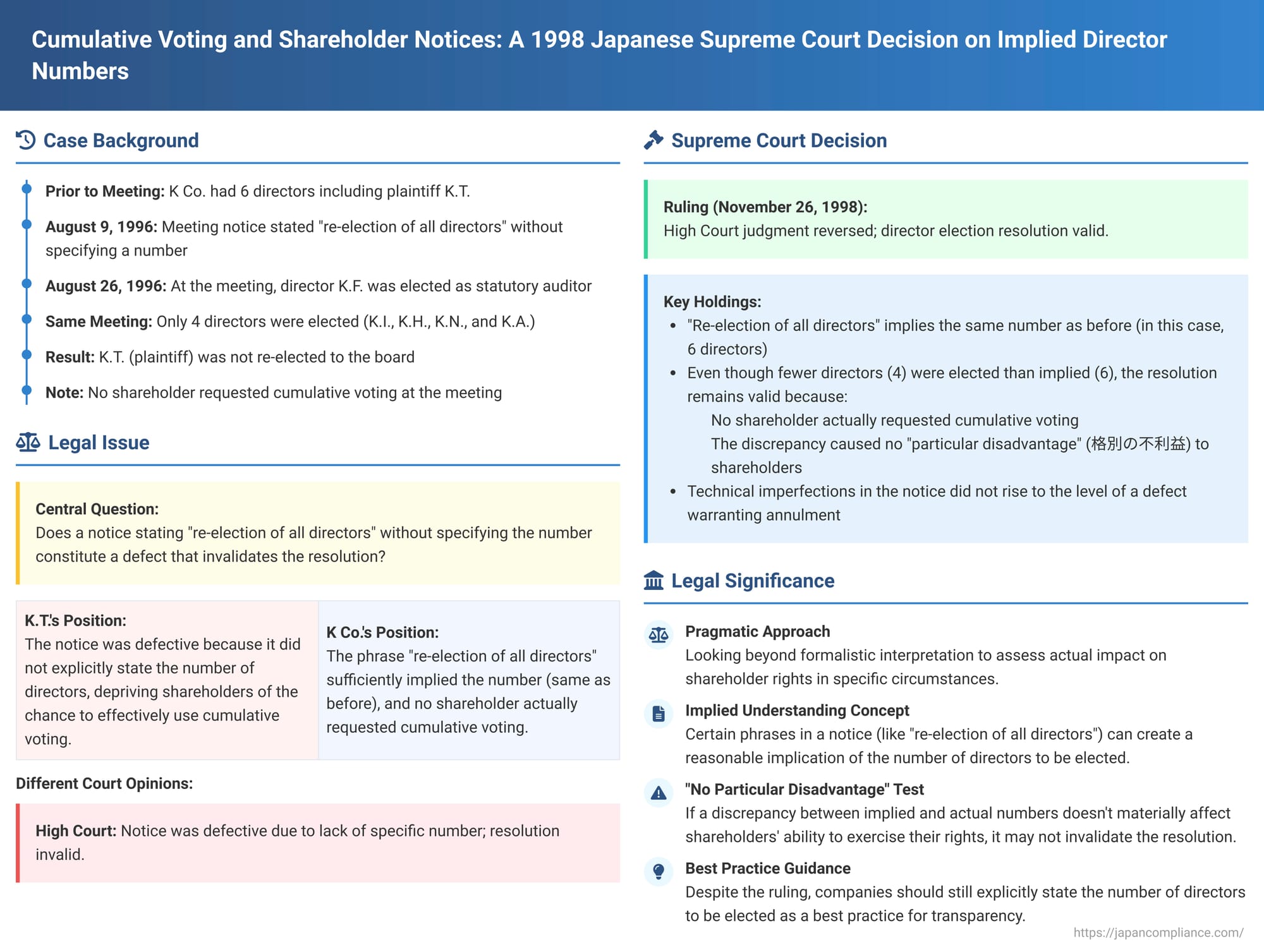

The case involved K.T., a shareholder and former director of K Co., who challenged the validity of a director election.

- K Co.'s articles of incorporation did not exclude the use of cumulative voting by its shareholders.

- The company's board previously consisted of six directors, one of whom was the plaintiff, K.T. Other directors included K.I. (the representative director), K.H., K.N., K.A., and K.F.

- The notice convening the annual general shareholders' meeting, dated August 9, 1996, for the meeting to be held on August 26, 1996, listed an agenda item as: "Agenda Item No. 2: Matter of re-election of all directors due to expiration of terms." The notice did not explicitly state the number of directors to be elected.

- Events at the Shareholders' Meeting:

- Before the election of directors, one of the incumbent directors, K.F., was elected as a statutory auditor and accepted this new position. This effectively removed K.F. from the pool of candidates for directorship.

- Subsequently, a resolution was passed to elect four individuals as directors: K.I., K.H., K.N., and K.A.

- The plaintiff, K.T., received insufficient votes and was not re-elected to the board.

- Importantly, no shareholder requested the use of cumulative voting for the director election.

- K.T. filed a lawsuit to annul the director election resolution, arguing that the convening notice was defective because it failed to specify the number of directors to be elected, thereby impairing his opportunity to request cumulative voting.

The Lower Courts' Diverging Views

The case saw differing opinions in the lower courts:

- First Instance Court: Dismissed K.T.'s claim, finding no actionable defect.

- High Court (on appeal): Sided with K.T. The High Court held that the convening notice was indeed defective because it did not explicitly state the number of directors to be elected. It reasoned that merely stating "re-election of all directors" was insufficient, especially since the number of directors ultimately elected (four) was less than the previous number (six), and one director had transitioned to an auditor role. This, in the High Court's view, invalidated the resolution.

The Supreme Court's Decision (November 26, 1998)

The Supreme Court, in a unanimous decision, overturned the High Court's ruling and found in favor of K Co.

Interpretation of "Re-election of All Directors"

The Court addressed the core issue of whether the notice was defective. It held that when a convening notice for a director election states an agenda item such as "Re-election of all directors due to expiration of terms," and provides no other specific number, it can generally be understood—in the absence of special circumstances—as implying that the company intends to elect the same number of directors as were previously serving on the board. In K Co.'s case, this meant the notice implied that six directors were to be elected. The Supreme Court found no special circumstances in this case to warrant a different interpretation.

Discrepancy Between Implied and Actual Numbers

The notice, as interpreted by the Supreme Court, implied that six directorships were to be filled. However, the events at the meeting unfolded differently:

- One incumbent director (K.F.) was appointed as an auditor, meaning she was no longer a candidate for a director position. This left five of the original six as potential candidates for directorship.

- Ultimately, only four directors were elected.

This created a discrepancy: the notice implied six positions, but effectively five individuals were considered as candidates for directorship, and only four were elected.

No Defect if No Prejudice and No Cumulative Voting Request

Despite this numerical inconsistency, the Supreme Court concluded that the convening notice was not defective and the resolution was valid. Its reasoning rested on two key observations specific to this case:

- No Request for Cumulative Voting: Crucially, no shareholder, including K.T., had actually requested the use of cumulative voting for the director election. The right, while available, was not invoked.

- No Particular Disadvantage to Shareholders: The Court determined that the discrepancy between the implied number in the notice (six) and the number of candidates deliberated upon (effectively five, after K.F. became an auditor) or the number actually elected (four) did not cause any "particular disadvantage" (格別の不利益 - kakubetsu no furieki) to the shareholders.

Because these two conditions were met—no request for cumulative voting and no particular disadvantage demonstrated—the Court found that the technical imperfection in the notice did not rise to the level of a defect warranting the annulment of the shareholders' resolution.

Analysis and Implications

The Supreme Court's 1998 decision offers a nuanced perspective on notice requirements when cumulative voting is a possibility.

- Pragmatic Approach: The ruling demonstrates a pragmatic approach, looking beyond a purely formalistic interpretation of notice requirements to assess the actual impact, or lack thereof, on shareholder rights and participation in the specific circumstances of the case.

- Implied Understanding vs. Explicit Statement: The Court accepted that certain phrases in a notice (like "re-election of all directors") can create a reasonable, implied understanding of the number of directors to be elected.

- The "No Particular Disadvantage" Test: This is a significant element of the decision. The general concern with electing fewer directors than stated (or implied) in a notice is that it can diminish the effectiveness of cumulative voting for minority shareholders; the fewer the seats, the more shares are needed to guarantee electing even one director. The Supreme Court, however, suggested that if this reduction doesn't actually alter the ability of minority shareholders to elect directors, or if no such cumulative voting is even attempted, the resolution might not need to be annulled. Academic commentary on this specific case pointed out that K.T. might have failed to secure re-election even if the full number of directorships (six) had been contested and filled.

- Guidance for Companies (and a Word of Caution): While K Co. prevailed in this instance, the decision should not be seen as a green light for companies to be lax in their convening notices. Relying on an implied number of directors and then deviating from it could still pose significant risks if, for example, a shareholder had made calculations for cumulative voting based on that implied higher number, or if they could demonstrate tangible prejudice from the discrepancy. The safest and most transparent practice for companies is always to explicitly state the number of directors to be elected, particularly when cumulative voting is not excluded by the articles of incorporation.

Conclusion

The Supreme Court's 1998 decision in the K Co. case clarified that a convening notice stating the "re-election of all directors due to expiration of terms" can, in the absence of other indicators, be understood to imply that the same number of directors as previously serving will be elected. More significantly, the Court indicated that a subsequent election of a slightly different number of directors might not automatically render the resolution void if cumulative voting was not requested by any shareholder and if the shareholders suffered no particular disadvantage as a result of the discrepancy.

This ruling balances the formal requirements for shareholder meeting notices with a substantive consideration of fairness and actual prejudice to shareholder rights. It underscores, however, the fundamental importance of clarity in such notices to ensure shareholders can effectively exercise all their rights, including the strategic use of cumulative voting.