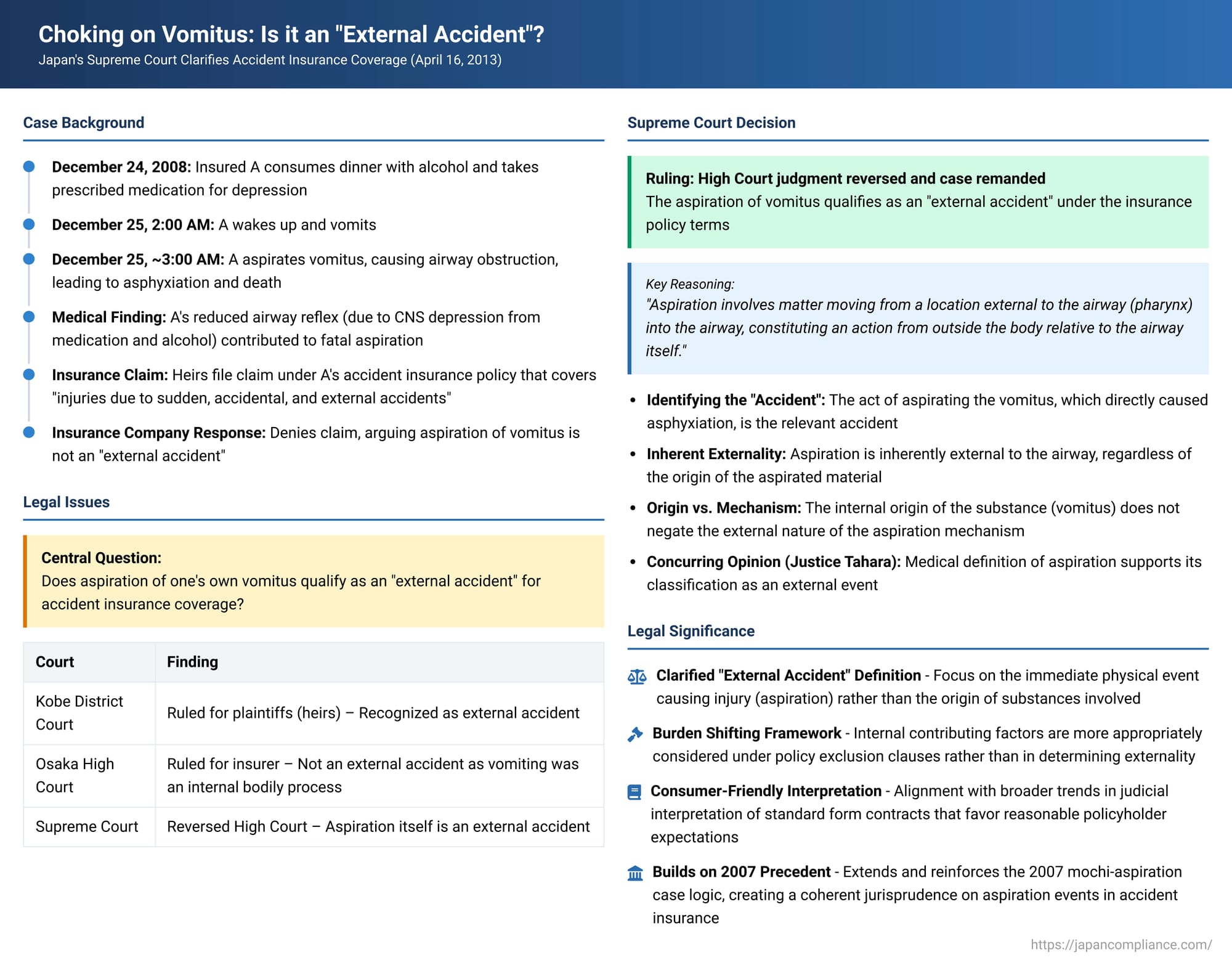

Choking on Vomitus: Is it an "External Accident"? Japan's Supreme Court Clarifies Accident Insurance Coverage

Judgment Date: April 16, 2013

Accident insurance policies are designed to provide financial protection against unforeseen injuries caused by external events. But what happens when the immediate cause of harm involves bodily substances, such as when an individual fatally chokes on their own vomitus? Is such a tragic event considered an "external accident" eligible for an insurance payout, or is it an internal event excluded from coverage? The Supreme Court of Japan addressed this complex issue in a significant judgment on April 16, 2013 (Heisei 23 (Ju) No. 1043), offering crucial clarification on the interpretation of "external accident" in accident insurance contracts.

The Tragic Incident and the Insurance Policy in Question

The case involved a man, A, who was insured under an ordinary accident insurance policy issued by Y Insurance Company. On December 24, 2008, A had dinner, which included the consumption of alcohol. He also took prescribed medication for the treatment of depression. Later that evening, A dozed off. Around 2:00 AM on December 25, he awoke and subsequently vomited. Tragically, A aspirated (inhaled) the vomitus, leading to an airway obstruction. Despite being rushed to a hospital, he died of asphyxiation shortly after 3:00 AM that morning.

Investigations revealed that the medication A had taken listed nausea and vomiting as potential side effects. Some of the drugs could also interact with alcohol, leading to central nervous system (CNS) depression, which in turn could impair sensory and motor functions. It was determined that A's asphyxiation resulted from a significantly diminished airway reflex, a condition brought about by the CNS depression and reduced bodily functions caused by the combined effects of the alcohol and medication he had consumed some hours before the fatal aspiration.

The accident insurance policy held by A contained several key provisions:

- Coverage Clause (ア): Y Insurance Company would pay insurance benefits for "injury suffered by the insured due to a sudden, accidental, and external accident."

- Illness Exclusion Clause (イ): Y Insurance Company would not pay for injury caused by the insured's "brain disease, illness, or mental derangement."

- Death Benefit Clause (ウ): If the insured suffered an injury as defined in clause (ア) and died as a "direct result" of that injury within 180 days of the accident (inclusive of the day of the accident), Y Insurance Company would pay a death benefit.

The Legal Dispute: Internal Bodily Process or External Accident?

Following A's death, his legal heirs (the plaintiffs, X et al.) filed a claim with Y Insurance Company for the death benefit under the policy. Y Insurance Company denied the claim, primarily arguing that A's death did not result from an "external" accident. The insurer's position was that the asphyxiation was due to an internal bodily process (vomiting and aspiration of stomach contents) influenced by substances A had voluntarily ingested, rather than an event caused by an external force acting upon his body.

The Kobe District Court, at the first instance, ruled in favor of X et al., ordering the insurer to pay. However, the Osaka High Court overturned this decision. The High Court reasoned that an "external accident" for insurance purposes must be an event where an external factor is the direct cause of the injury. It opined that accidents resulting from internal bodily changes or malaise—even if those changes are influenced by substances like drugs or alcohol ingested by the insured—do not meet this criterion of externality. Since A's fatal asphyxiation was caused by depressed airway reflexes stemming from the effects of ingested alcohol and medication, the High Court concluded it was not directly caused by an external action and thus not covered. X et al. subsequently appealed this decision to the Supreme Court.

The Supreme Court's Interpretation of "External Accident"

The Supreme Court reversed the Osaka High Court's judgment and remanded the case for further proceedings. The Court's interpretation of "external accident" was pivotal:

- Definition of "External Accident": The Court began by reaffirming a principle from a previous ruling (Supreme Court, July 6, 2007, Heisei 19 (Ju) No. 95, a case involving an elderly person with Parkinson's disease who fatally choked on mochi): an "external accident," according to its literal meaning in such policy clauses, refers to an accident caused by an action or force originating from outside the insured's body.

- Identifying the "Accident" in This Case: The policy stipulates that the "accident" must be one that can cause bodily injury to the insured. The Supreme Court identified the act of aspirating the vomitus, which directly led to A's asphyxiation and death, as the "accident" in question.

- Aspiration as an Inherently External Event: This was the crux of the Court's reasoning. "Aspiration" (誤嚥 - goen) is the medical term for the entry of ingested or regurgitated matter into the trachea (windpipe) instead of its proper path down the esophagus (food pipe). The Court stated that this process of matter moving from a location effectively external to the airway (such as the pharynx, after vomiting) into the airway inherently involves an "action from outside the body" relative to the airway itself. Therefore, the act of aspiration itself qualifies as an "external accident" under the terms of the policy.

- Origin of Aspirated Material Does Not Negate Externality: Crucially, the Supreme Court clarified that this principle holds true even if the substance that caused the airway obstruction (the aspirated material) was originally the insured's own stomach contents (i.e., vomitus). The internal origin of the substance does not change the "external" nature of the event of that substance improperly entering the airway. The focus is on the injurious mechanism – the physical act of foreign matter (in this context, foreign to the airway) breaching the airway's defenses.

Justice Mutsuo Tahara, in a concurring opinion, reinforced this view. He noted that the High Court likely doubted the externality because the aspirated material was vomitus. However, he emphasized that medically, aspiration refers to any liquid or solid improperly entering the trachea during swallowing or regurgitation. The act of aspiration is, in itself, an external event, regardless of whether the material originated from oral intake, vomit (including vomited blood), or even sources within the oral cavity like bleeding or tooth fragments.

Broader Context: Interpreting Insurance Policies and the "Externality" Requirement

The "external accident" requirement in accident insurance policies serves the fundamental purpose of distinguishing injuries caused by accidents from those caused by illness or internal bodily degeneration, which are typically covered by different types of insurance (like health or life insurance with illness riders).

The Supreme Court's decision in this 2013 vomitus aspiration case, building upon its 2007 mochi-aspiration precedent, signals a specific approach to interpreting "externality." It tends to focus on the immediate physical event causing the injury (the act of aspiration) as the "accident." This approach avoids getting too entangled in the insured's pre-existing conditions or internal states (like the effects of medication or alcohol) when initially determining if an 'external accident' occurred.

Instead, such internal conditions or pre-existing illnesses are more appropriately considered under specific policy exclusion clauses, such as the common clause excluding coverage for injuries "caused by ... illness." A significant implication of this interpretive approach is that it effectively places the burden of proof on the insurer to demonstrate that such an exclusion applies, rather than requiring the claimant to prove the absence of any internal contributing factors as part of establishing the "externality" of the accident.

This can be seen as consistent with broader trends in judicial interpretation of standard form contracts, including insurance policies. Courts sometimes adopt interpretations that align with the reasonable expectations of the policyholder or construe ambiguous terms in a manner that does not unduly disadvantage the consumer, especially given the inherent information asymmetry and disparity in bargaining power between individual policyholders and insurance companies.

Implications of the Ruling and the Remand

The Supreme Court's judgment established a clear legal principle: the aspiration of vomitus can satisfy the "external accident" requirement for an accident insurance claim. By defining the aspiration itself as the external event, the Court provided a pathway for potential coverage in such distressing circumstances.

The case was remanded to the Osaka High Court for further proceedings. This meant the High Court had to re-evaluate X et al.'s claim, now accepting the Supreme Court's determination that the aspiration of vomitus constituted an "external accident." However, this did not automatically guarantee payment of the insurance claim. On remand, the High Court would need to consider other elements of the policy and the facts, including:

- Whether the aspiration was "sudden" and "accidental" (which it likely was).

- Whether A's death was a "direct result" of the injury sustained from the aspiration.

- Most importantly, whether the illness exclusion clause applied. The influence of A's prescribed medication for depression and the ingested alcohol, which contributed to the suppressed airway reflexes and led to the vomiting and aspiration, would be central to this determination. The insurer (Y) would bear the burden of proving that A's death was caused by "illness" or "mental derangement" (potentially linked to the depression or the effects of its treatment interacting with alcohol) to the extent that the exclusion should apply.

Ongoing Complexities in Accident Insurance Interpretation

While this Supreme Court ruling provides significant clarification regarding the "externality" of aspiration events, the broader field of accident insurance interpretation, particularly concerning causation, remains complex. Cases where multiple factors—such as an external event, an underlying internal health condition, and lifestyle choices (like alcohol consumption)—converge to cause injury or death often require nuanced legal analysis. Defining the precise boundaries between a covered "external accident" and an excluded "illness-caused" event continues to be a subject of legal debate and judicial scrutiny, with outcomes often depending heavily on the specific facts of each case and the precise wording of the insurance policy in question.

Conclusion

The Supreme Court's 2013 decision in the vomitus aspiration case represents an important development in Japanese accident insurance law. By focusing on the physical event of aspiration as an "external accident," regardless of the internal origin of the aspirated substance, the Court adopted an interpretation that potentially broadens coverage for policyholders in certain tragic circumstances. The ruling underscores that the primary inquiry for "externality" should be the nature of the injurious event itself, with internal contributing factors often being more relevant to the application of specific policy exclusion clauses. This decision provides valuable guidance for insurers, policyholders, and legal practitioners navigating the complexities of accident insurance claims.