What Specific Actions Qualify as "Working" (Jisshi) a Patented Invention in Japan? In the realm of Japanese patent law, the concept of "working" (実施 - jisshi) an invention is central to determining whether patent infringement has occurred. A patent grants its owner the exclusive right to work the patented invention in the course of trade (Article 68, Japanese Patent Act)

What Constitutes Indirect Patent Infringement Under Japanese Law, and How Can It Be Proven? Japanese patent law, like that of many other industrialized nations, recognizes that the effective enforcement of patent rights requires more than just addressing direct acts of infringement. Often, the most commercially significant or easiest party to pursue is not the end-user directly infringing the patent, but rather a supplier or

When Can the Doctrine of Equivalents Expand Patent Protection Beyond Literal Infringement in Japan? In the landscape of Japanese patent litigation, the question of infringement primarily hinges on whether an accused product or process falls within the literal wording of the patent claims. However, Japanese law recognizes that a strict, purely literal application of claim language might sometimes allow an infringer to make insubstantial

How Are Patent Claims Interpreted in Japanese Infringement and Revocation Proceedings? The interpretation of patent claims stands as a cornerstone in Japanese patent litigation, whether in the context of an infringement suit or during proceedings to determine a patent's validity, such as a revocation trial (often an invalidity contention within an infringement suit). The claims define the exclusive rights

What Are the Core Issues Litigated in a Japanese Patent Infringement Lawsuit? Navigating a patent infringement lawsuit in Japan requires a thorough understanding of several core legal and factual questions that form the battleground between patentees and alleged infringers. These lawsuits are not monolithic; they involve a structured examination of distinct issues, each carrying its own set of rules, precedents, and strategic

Inherited Property Disposed of Before Division? How Japan's New Rules Address Unauthorized Sales by Co-Heirs The period between an individual's death (commencement of inheritance) and the final division of their estate (遺産分割 - isan bunkatsu) can be a vulnerable time for estate assets. During this phase, the inherited property is co-owned by all heirs (共同相続 - kyōdō sōzoku), each holding an undivided interest.

Estate Division Taking Too Long? How Japan's New Rules Clarify When "Partial Estate Division" is Possible The process of estate division (遺産分割 - isan bunkatsu) in Japan, where co-heirs determine how the deceased's assets will be distributed among them, can sometimes be a lengthy and complex undertaking. While the traditional goal is often a comprehensive, one-time settlement of the entire estate, practical realities can

Estate Planning for Long-Married Couples in Japan: What is the New Presumption for Gifts or Bequests of Residential Property Between Spouses of 20+ Years? In Japanese inheritance law, the principle of fairness among heirs often involves a "clawback" mechanism for certain lifetime gifts or bequests made by the deceased to individual heirs. These "special benefits" (特別受益 - tokubetsu jueki), such as significant gifts for marriage, starting a business, or substantial

Securing Inherited Assets in Japan: What are the New "Perfection Requirements" for Asserting Rights to Inherited Property Against Third Parties? When an individual in Japan passes away leaving multiple heirs, the co-inherited estate can present complexities, particularly when it comes to how those heirs can definitively assert their rights to specific assets against third parties, such as purchasers or creditors. Historically, there were areas of uncertainty regarding what steps an

Navigating Will Execution in Japan: What are the Key Clarifications and Changes to the Executor's Powers and Responsibilities? The role of a will executor (遺言執行者 - igon shikkōsha) is pivotal in ensuring that a deceased person's testamentary wishes are carried out accurately and efficiently. In Japan, the executor acts as the legal representative responsible for administering the estate according to the terms of the will. Recognizing

Beyond Heirs: How Does Japan's New "Special Contribution" System Recognize the Efforts of Non-Heir Relatives in Maintaining or Increasing the Deceased's Estate? Japanese inheritance law has traditionally centered on the rights of legal heirs. While a system known as kiyobun (寄与分 – contributor's portion) has existed to recognize special contributions made by heirs that helped maintain or increase the deceased's estate, a significant gap remained: what about non-heir relatives

Accessing Bank Accounts After Death in Japan: How Has the New Law Changed the Rules for Withdrawing Deposits Before Estate Division is Finalized? When an individual passes away in Japan, their bank accounts are typically frozen by financial institutions upon notification of death. While this is a measure to protect the deceased's assets until inheritance is formally settled, it has historically created significant practical difficulties for heirs needing immediate access to

Making Wills Easier and Safer in Japan: Understanding the Relaxed Rules for Holographic Wills and the New Public Custody System Wills are a fundamental tool in estate planning, allowing individuals to determine the distribution of their assets after their passing. In Japan, several forms of wills are recognized, including notarized wills (公正証書遺言 - kōsei shōsho igon), secret-deed wills (秘密証書遺言 - himitsu shōsho igon), and holographic wills (自筆証書遺言 - jihitsu shōsho

Japan's Inheritance Law Overhaul: What Does the Shift to Monetary Claims for "Legally Secured Portions" (Iryubun) Mean for Heirs and Business Succession? Japan's system of "Legally Secured Portion" (遺留分 - Iryūbun) is a cornerstone of its inheritance law, designed to guarantee a minimum share of an estate for certain close heirs, irrespective of the deceased's will. Historically, the enforcement of these rights often led to complex

How Does Japan's "Short-Term Spousal Residency Right" Protect Surviving Spouses Immediately After Inheritance Commences? The period immediately following the death of a spouse is fraught with emotional and practical challenges. Among these is the critical question of housing security for the surviving spouse, particularly if the marital home was owned by the deceased. Recognizing this vulnerability, Japan's revised Civil Code, with key

What are Japan's New "Spousal Residency Rights" and How Do They Impact Long-Term Housing Security for Surviving Spouses? The Japanese Civil Code underwent significant revisions concerning inheritance law, with many changes taking effect progressively. Among the most impactful of these reforms is the introduction of "Spousal Residency Rights" (配偶者居住権 - haigūsha kyojūken), specifically designed to enhance the housing security of a surviving spouse. These rights came

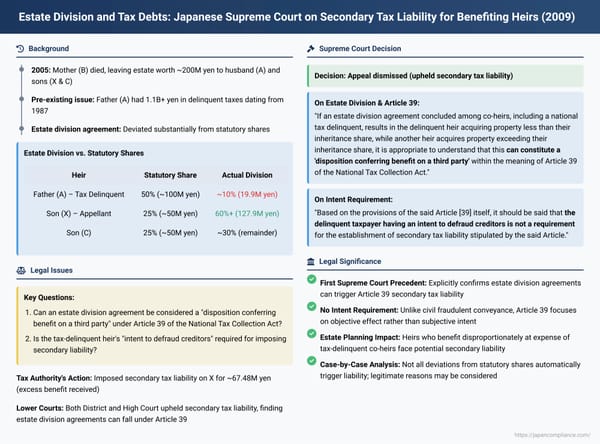

Estate Division and Tax Debts: Japanese Supreme Court on Secondary Tax Liability for Benefiting Heirs Judgment Date: December 10, 2009 In a significant decision clarifying the reach of tax collection powers into estate settlements, the First Petty Bench of the Supreme Court of Japan ruled that an estate division agreement can trigger secondary tax liability for an heir who benefits at the expense of a

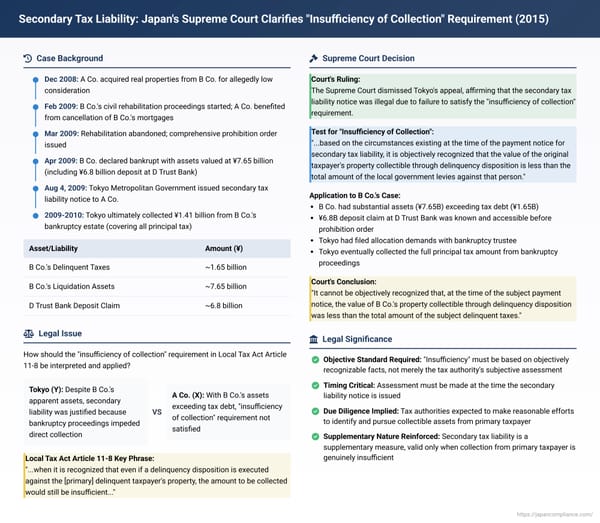

Secondary Tax Liability: Japan's Supreme Court Clarifies "Insufficiency of Collection" Requirement Judgment Date: November 6, 2015 In a significant decision for understanding the prerequisites for imposing secondary tax liability, the Second Petty Bench of the Supreme Court of Japan provided a crucial interpretation of the "insufficiency of collection" requirement under local tax law. The case involved the Tokyo Metropolitan

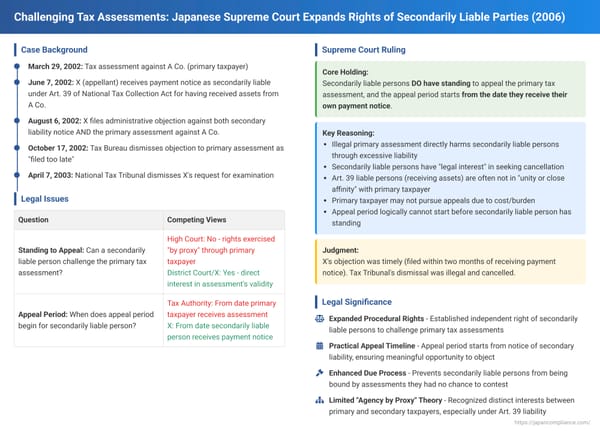

Challenging Tax Assessments: Japanese Supreme Court Expands Rights of Secondarily Liable Parties Judgment Date: January 19, 2006 In a significant decision for Japanese tax procedure, the First Petty Bench of the Supreme Court of Japan clarified and expanded the rights of individuals and entities held secondarily liable for another taxpayer's delinquent taxes. The Court ruled that such secondarily liable parties

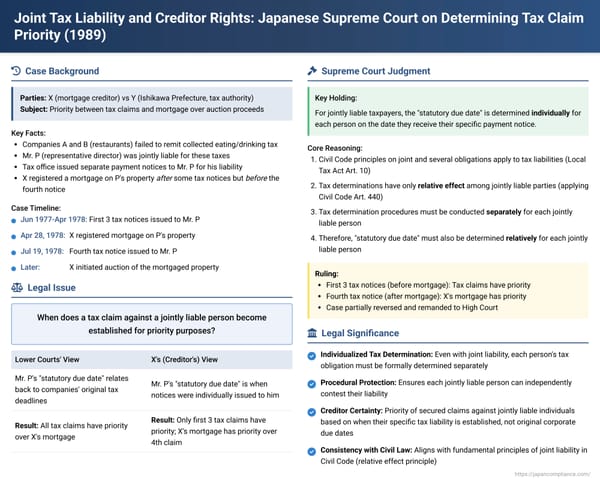

Joint Tax Liability and Creditor Rights: Japanese Supreme Court on Determining Tax Claim Priority Judgment Date: July 14, 1989 In a pivotal decision clarifying the rights of creditors in relation to tax claims against individuals who are jointly and severally liable for taxes primarily owed by other entities (such as corporations they manage), the Second Petty Bench of the Supreme Court of Japan addressed

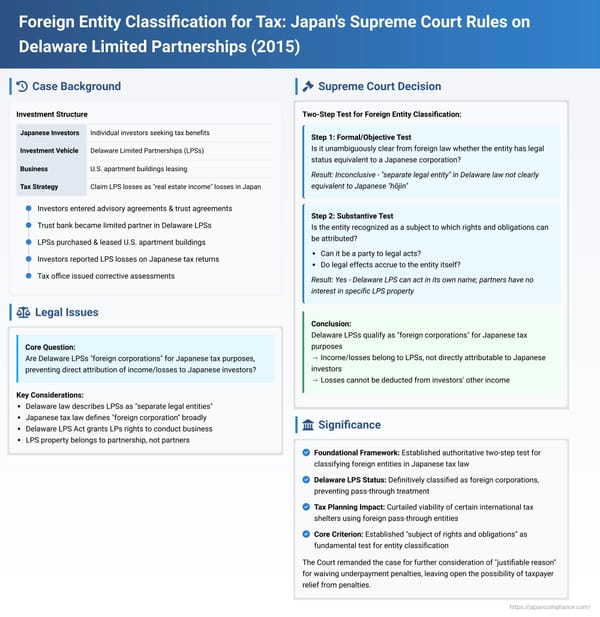

Foreign Entity Classification for Tax: Japan's Supreme Court Rules on Delaware Limited Partnerships Judgment Date: July 17, 2015 In a landmark decision with significant implications for Japanese investors in foreign entities and for international tax planning, the Second Petty Bench of the Supreme Court of Japan established a crucial two-step framework for determining whether a foreign-organized entity should be treated as a "

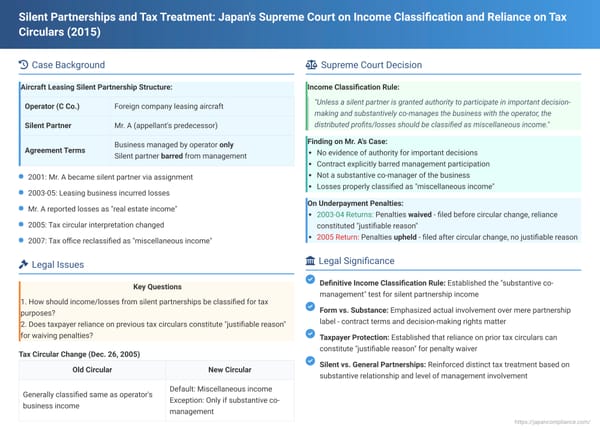

Silent Partnerships and Tax Treatment: Japan's Supreme Court on Income Classification and Reliance on Tax Circulars Judgment Date: June 12, 2015 In a closely watched decision with significant implications for investors in silent partnerships (tokumei kumiai - 匿名組合), the Second Petty Bench of the Supreme Court of Japan clarified how income or losses distributed to individual silent partners should be classified for income tax purposes. The

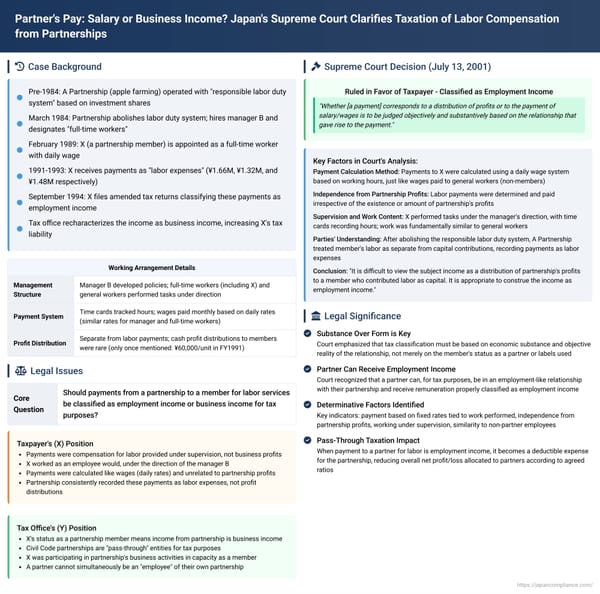

Partner's Pay: Salary or Business Income? Japan's Supreme Court Clarifies Taxation of Labor Compensation from Partnerships Judgment Date: July 13, 2001 In a significant ruling that delves into the nuanced tax classification of payments made by a Civil Code partnership to one of its members for labor services, the Second Petty Bench of the Supreme Court of Japan provided crucial guidance. The case centered on whether

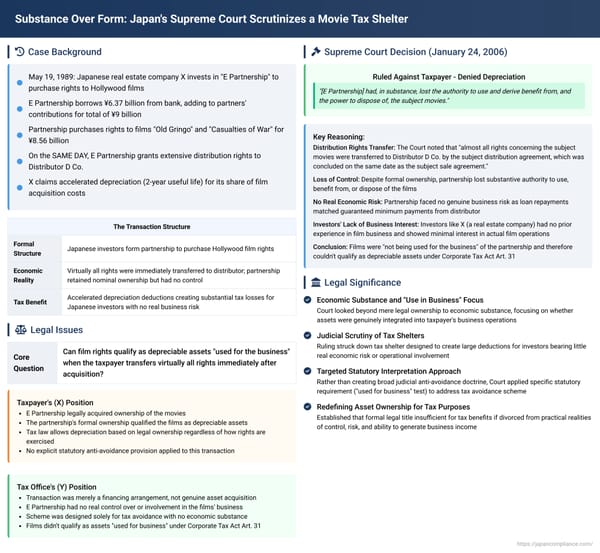

Substance Over Form: Japan's Supreme Court Scrutinizes a Movie Tax Shelter Judgment Date: January 24, 2006 In a significant decision impacting the landscape of tax shelters in Japan, the Third Petty Bench of the Supreme Court delivered a judgment in what is often referred to as the "Palazzina Case" (though this specific name is not used in the judgment

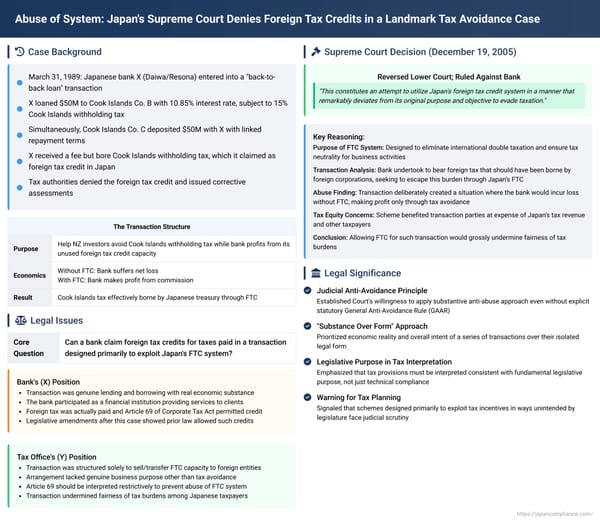

Abuse of System: Japan's Supreme Court Denies Foreign Tax Credits in a Landmark Tax Avoidance Case Judgment Date: December 19, 2005 In a highly influential decision concerning international tax avoidance, the Second Petty Bench of the Supreme Court of Japan denied a major Japanese bank the benefit of foreign tax credits arising from a complex "back-to-back loan" transaction. The Court, looking beyond the formal